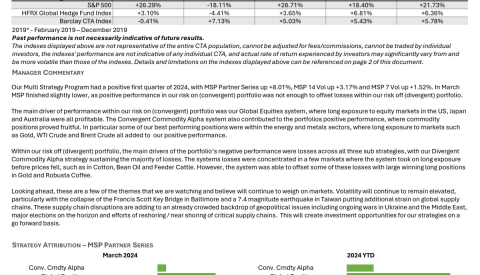

Managed Futures Dashboard:

Top Managed Futures News, Listings, Member Posts, Managed Futures Daily Indices and more!

ETF use among actively managed mutual fund portfolios

- D. Eli Sherrill, Sara E. Shirley, Jeffrey R. Stark

- Journal of Financial Economics

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the research questions?

As of 2017, and in spite of the documented negative relationship between fund performance and use of ETFs, approximately one-third of US-domiciled, actively managed mutual funds held ETFs at one time or another. Active managers justifiably make use of ETFs to improve their portfolio management operations. But is their use for cash management, liquidity, improved returns, or risk reduction? The answer depends on the purpose as well as the type of ETF: benchmarked or non-benchmarked. Using a sample of US-domiciled active mutual funds observed between 2004 and 2015, the authors of this research are able to tease out the unique benefits that the use of benchmarked vs. non-benchmarked ETFs provides.

- Does the use of ETFs by mutual funds improve liquidity management?

- Does the use of benchmark ETFs reduce portfolio risk?

- Does the use of non-benchmark ETFs increase fund return performance?

- Does the use of non-benchmark ETFs reduce portfolio risk?

What are the Academic Insights?

- YES. Mutual Funds use benchmark ETFs to reduce cash, especially if it is a result of large fund inflows. The exchange of cash holdings earning the risk-free rate, with shares of an ETF earning the benchmark return, reduces tracking error and cash drag significantly. The assumption in this research is that benchmark ETFs are highly liquid and mutual funds prefer those exhibiting the greatest liquidity. This proposition is confirmed. The data shows that benchmark ETFs tend to be larger, exhibit higher trading volume, and smaller bid-ask spreads. Of those benchmark ETFs, mutual funds select those that are the largest and most heavily traded and exhibit the smallest bid-ask spreads. The preference for highly liquid ETFs on the part of mutual funds is consistent with their need for managing cashflow within the fund. As shown in Table 6 below, the use of benchmark ETFs is associated with a reduction of cash flows, along the lines of a 13.47% decline in the average cash position during the relevant month—where the average ETF user maintains a cash position of 2.97%. Large flows into the fund are related to ETF trading. In general, for each 1% increase (decrease) in fund flows, the authors observe a .40% (.06%) decrease (increase) in cash holdings. However, if the fund holds benchmark ETFs, those numbers are changed by 40%. Quite a change in magnitude. The beneficial effects are obvious: inflows are invested immediately at the benchmark return. There was no similar impact for mutual funds using non-benchmark ETFs.

- YES. Tracking error is indeed reduced for mutual funds holding benchmark ETFs—monthly tracking error is 1.41% vs. 1.53% for those holding non-benchmark ETFs. This is a substantial difference on an annualized basis, approximately 2% lower. Although at those monthly rates the differences in annualized tracking error are swamped by the magnitude of approximately 22% to 24%. Assuming (annual TE = monthly TE * Sqrt(250)) of the risk measure itself. Can it really be that large when annualized? Whew.

- NO. The authors report no empirical relationship between the use of non-benchmark ETFs and mutual fund returns. Several types of returns are calculated including benchmark excess returns, style (either size or book-to-market) excess returns, objective excess returns (when matched with the CRSP fund objective), raw returns, and as a four-factor (Fama-French, Carhart) alpha. Fund performance was unaffected in either a positive or negative direction, with the exception for micro-cap objective mutual funds where a weak improvement in objective excess returns and four-factor alpha was observed.

- YES. A number of comparisons of return volatility were made including (1) Mutual funds using non-benchmark ETFs vs. mutual funds that use no ETFs at all; (2) Mutual funds that use non-benchmark ETFs vs the average of all non-ETF users; and (3) Non-benchmark users vs. benchmark ETF users. A significant reduction in monthly volatility was observed in all three cases. For example, in the first case, a reduction from 4.85% to 4.48% in monthly volatility was reported. Non-benchmark users exhibited lower volatility than non-user mutual funds and benchmark users. The results provide direct evidence for the notion that mutual funds exhibit a diversification benefit from using non-benchmark ETFs as opposed to an improvement in returns. The authors provide evidence that it is specifically the use of non-benchmark ETFs that is key. With non-benchmark stocks, the mutual fund obtains exposure to stocks not held by the fund, while holding benchmark ETFs simply increases exposure to stocks already included in the mutual fund portfolio.

Why does it matter?

This paper contributes to the literature on the use of passive investment vehicles, like ETFs, by clarifying the range of benefits available to active managers from their use. The specific examination of improved cash management, enhanced performance, and improved diversification are all cases that justify the utilization of ETF products.

The most important chart from the paper

- The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.Abstract

It is well known that actively managed mutual funds use exchange-traded funds (ETFs), although current research has yet to establish the benefits of these positions. Focusing on ETF type, we investigate whether or not ETFs impact portfolio management. Funds using benchmark ETFs see reductions in cash holdings, particularly during periods of large flows, and lower tracking error. In contrast, non-benchmark ETF positions improve the performance of large mutual funds investing in micro-cap stocks while also reducing portfolio risk. While studies caution against the extensive use of ETFs, we conclude that ETFs can provide tangible benefits for funds when considering the type of ETF used.

How Active Mutual Funds Use ETFs was originally published at Alpha Architect. Please read the Alpha Architect disclosures at your convenience.

Today's Managed Futures Headlines:

Access Over 250K+ Industry Headlines, Posts and Updates

Join AlphaMaven

The Premier Alternative Investment

Research and Due Diligence Platform for Investors

Free Membership for Qualified Investors and Industry Participants

- Easily Customize Content to Match Your Investment Preferences

- Breaking News 24/7/365

- Daily Newsletter & Indices

- Alternative Investment Listings & LeaderBoards

- Industry Research, Due Diligence, Videos, Webinars, Events, Press Releases, Market Commentary, Newsletters, Fact Sheets, Presentations, Investment Mandates, Video PitchBooks & More!

- Company Directory

- Contact Directory

- Member Posts & Publications

- Alpha University Video Series to Expand Investor Knowledge

- AUM Accelerator Program (designed for investment managers)

- Over 450K+ Industry Headlines, Posts and Updates