A Call On $UBER

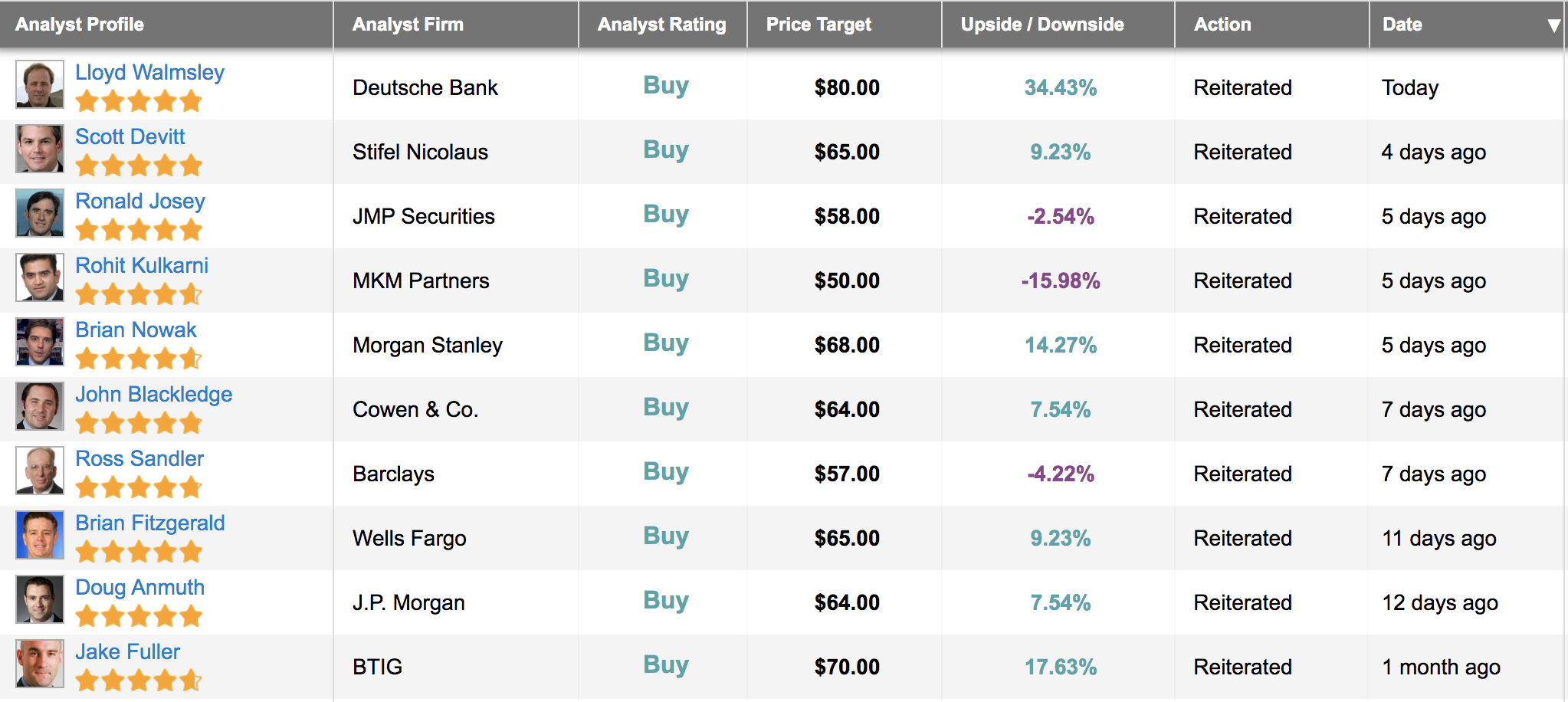

Lloyd Walmsley from Deutsche Bank has today placed a buy recommendation on UBER technologies with a price target of $80 per share. This follows a week where six other big banks have placed buy recommendations on the stock. UBER has gained 12.39% in the past week's trading.

With the earnings release due February the 10th, I thought I'd provide a rundown on the company's stock.

expansionary phase

e-hailing has consolidated itself as an innovation, which is here to stay. The industry is in an expansionary phase where investment is growing rapidly, ancillary services such as Uber & Lyft rentals are growing, and cost-cutting is taking place.

Also, and possibly the most noticeable news recently is the expansion of UBER EATS with the acquisition of Drizly, the alcohol delivery company is being acquired for $ 1.1 billion in stock and cash. Drizly is said to have increased gross bookings by an average of 300% year over year since inception in 2012. Tom White from D.A. Davidson calls this interesting and exciting as UBER now diversifies into consumer discretionary.

Possibly breaking by the end of 2021

Morgan Stanley sees a path for UBER to break-even in 2021 due to cost-cutting and a sharp recovery in consumer demand, with the company eventually returning to pre-covid user levels in early 2022.

Source: Finbox

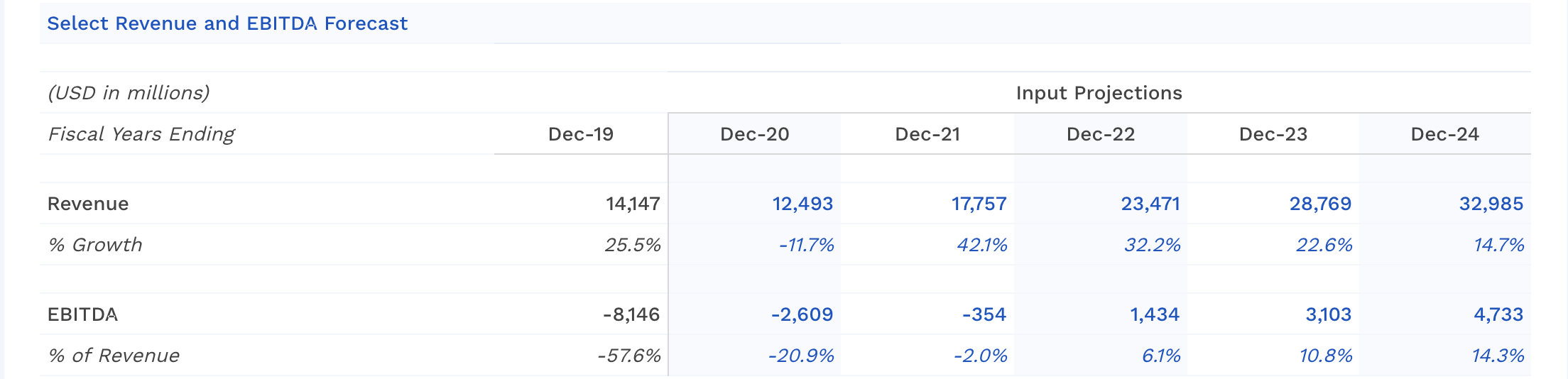

The expectation is that revenue growth will be at 42% in 2021 as we see a snapback in consumer usage while the vaccine gets rolled out. According to the company itself, Uber has also been able to cut costs significantly, with the main driver being contracting their drivers on a contract basis instead of a full-time basis.

Q 4 Earnings expectations

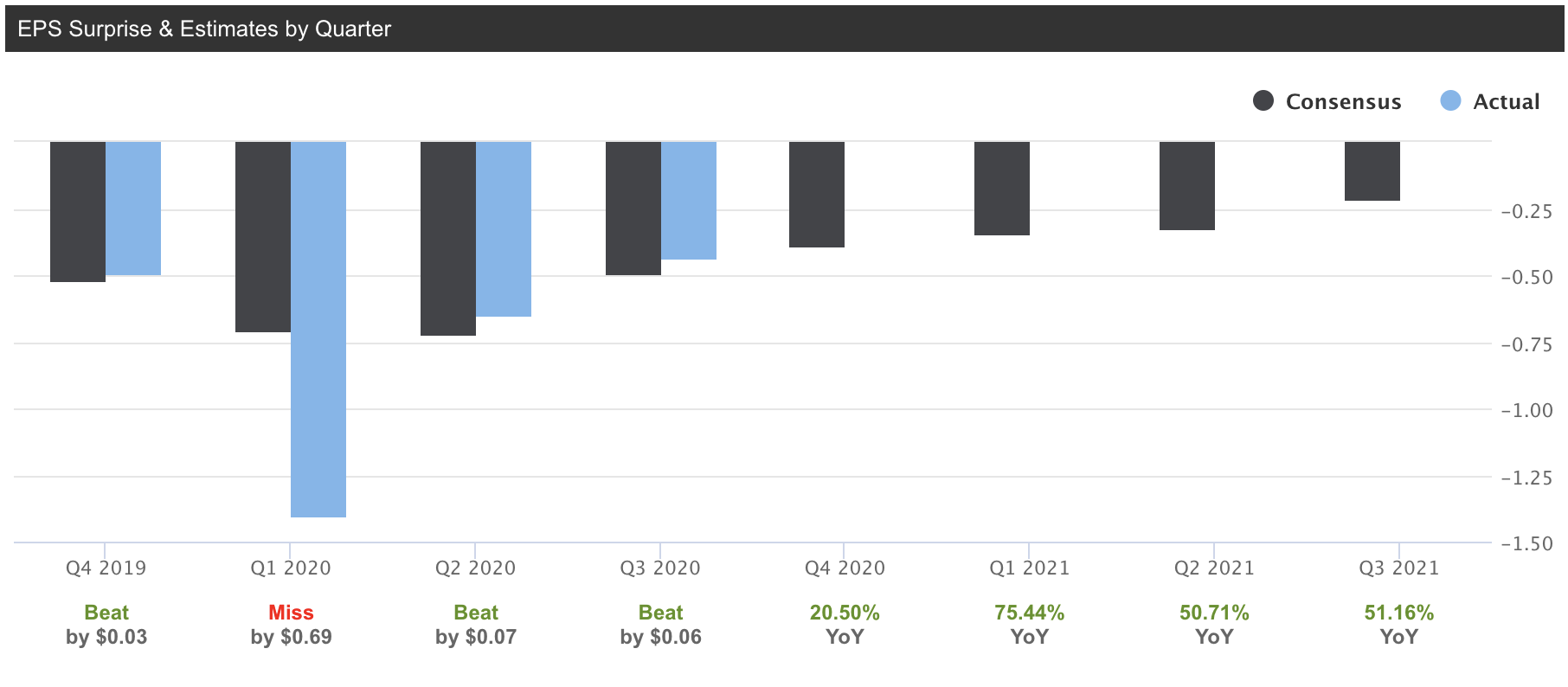

According to Estimize 49, analysts expect revenue to be around $4.035 billion for UBER, versus $3 billion in 2019's fourth quarter. FactSet has 28 analysts reporting that the company will post a loss of 67 cents per share versus the expected loss at the start of the quarter being 76 cents per share.

Source: Seeking Alpha

Uber has a history of beating EPS estimates, and Seeking Alpha believes that growth of 20.50% year on year might see this being the case again.

Investors should consider that UBER uses non-GAAP accounting when reporting adjusted net-revenue at times, and we might see a similar case on Wednesday as there's an apparent tilt in consumer demand between pre-vaccine and post-vaccine times.

Valuation & Price targets

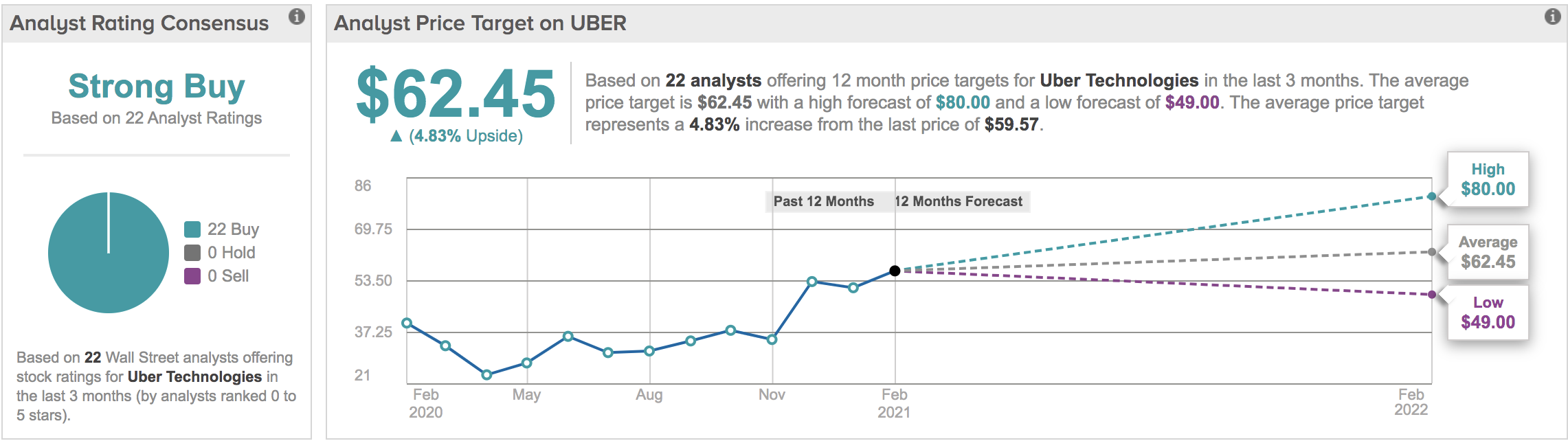

Optimists believe Uber will trade between $62.45 and $80 per share. TipRanks also reports that hedge funds bought 18.2 million shares in the last quarter. Hedge fund activity hasn't cooled off since Tiger Global's manager Chase Coleman revealed the fund's large stake in UBER at the end of 2019. Most funds must've looked through the pandemic betting that consumer levels will return to normal as lockdowns eased, according to TipRanks Hedge funds now hold more than 70 million of UBER's 1.85 billion shares outstanding, that's near 7x the amount held by hedge funds in December 2019.

Source: TipRanks

As for institutional buy recommendations, UBER holds a 10/10 score for the last ten recommendations.

Source: Tipranks

Lloyd Walmsley from Deutsche Bank is the latest analyst who's set a price target of $80, as he believes UBER will be over the levels they were in Q4 2019. Walmsley says Deutsche Bank as a whole believes that UBER can increase efficiency in the food delivery space by using the subscription-based model.

Risks

The stock's trading at a high price to book value 3.4x as UBER is still in the growth phase of the industry life cycle From my side I have further concerns regarding the stocks ability to sustain short-term growth during large acquisitions such as Drizly as it offloads cash off the balance sheet for more stocks of companies who're also trading at high multiples.

Lastly, the food delivery business is undoubtedly very competitive. Although UBER remains the prominent figure in the e-hailing business, there will indeed be established delivery companies currently exploiting other industries that might make moves into the e-hailing space.

My take

Although consumer discretionary is in a bad spot, I believe UBER reaching the $80 price target seems realistic due to a growing increased top-line, EBITDA, levered free cash flow. The mentioned is all driven by e-hailing consolidating itself, UBER's diversification into other markets, the acquisition of Drizly, and the fact that the stock has been waiting in the wings to be freed up; in my opinion, 2021 is the year that may well happen.