PopReach (POPR) A Stock To Watch As It Presents Value & Growth In The Mobile Gaming Space.

PopReach Corporation operates as a free-to-play mobile game publisher in North America, Europe, Australia, and internationally. It focuses on acquiring subsidiaries, with the prospect of abnormal scale. The company owns 12 game franchises, including Smurfs’ Village, Kitchen Scramble, Gardens of Time, City Girl Life, War of Nations, and Kingdoms of Camelot. The company is headquartered in Toronto, Canada.

Free Online Mobile Games Industry Growth

Online mobile games CAGR is predicted to be 14% between 2020-25 and in addition to industry growth in-app-purchases are predicted to grow at 19.8% per year between 2020-2027, and add-revenue is expected to grow at 13% year on year (Statista, 2020).

According to With 5G powering advancements in cloud-gaming it’s expected that mobile gaming will continue to outpace PC gaming, as hardcore gamers increase their usage of mobile gaming subscription-based revenue will enter the fray, both apple and google unveiled subscription programs in 2019.

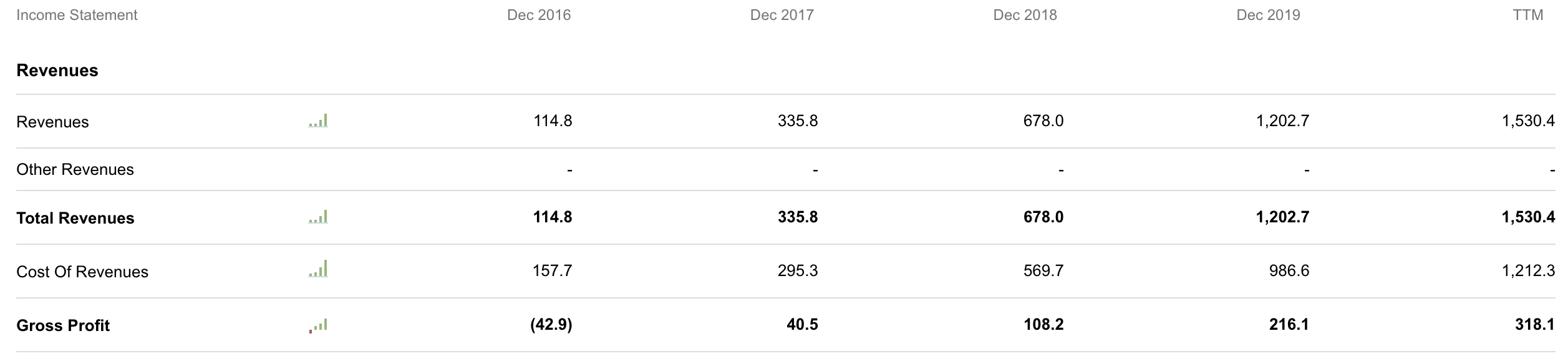

Revenue Growth, Cost Cutting, and Earnings

Source: Finbox

A couple of factors to note with Popreach is that core revenue reported for Q3 2020 outweighed add-revenue by 27.68 times, along with steady revenue growth in both 9-months reported and for Q3.

The second factor, which is a key determining factor to our investment decisions is cost-cutting. The company is seeking subsidiaries who’ve significant abilities to cut costs. The company is achieving this through cross-platform development, as acquiring company synergies between underlying companies are increasing, which allows for outsourcing, price reductions in services, as well as reduced cumulative employee wages (less hiring).

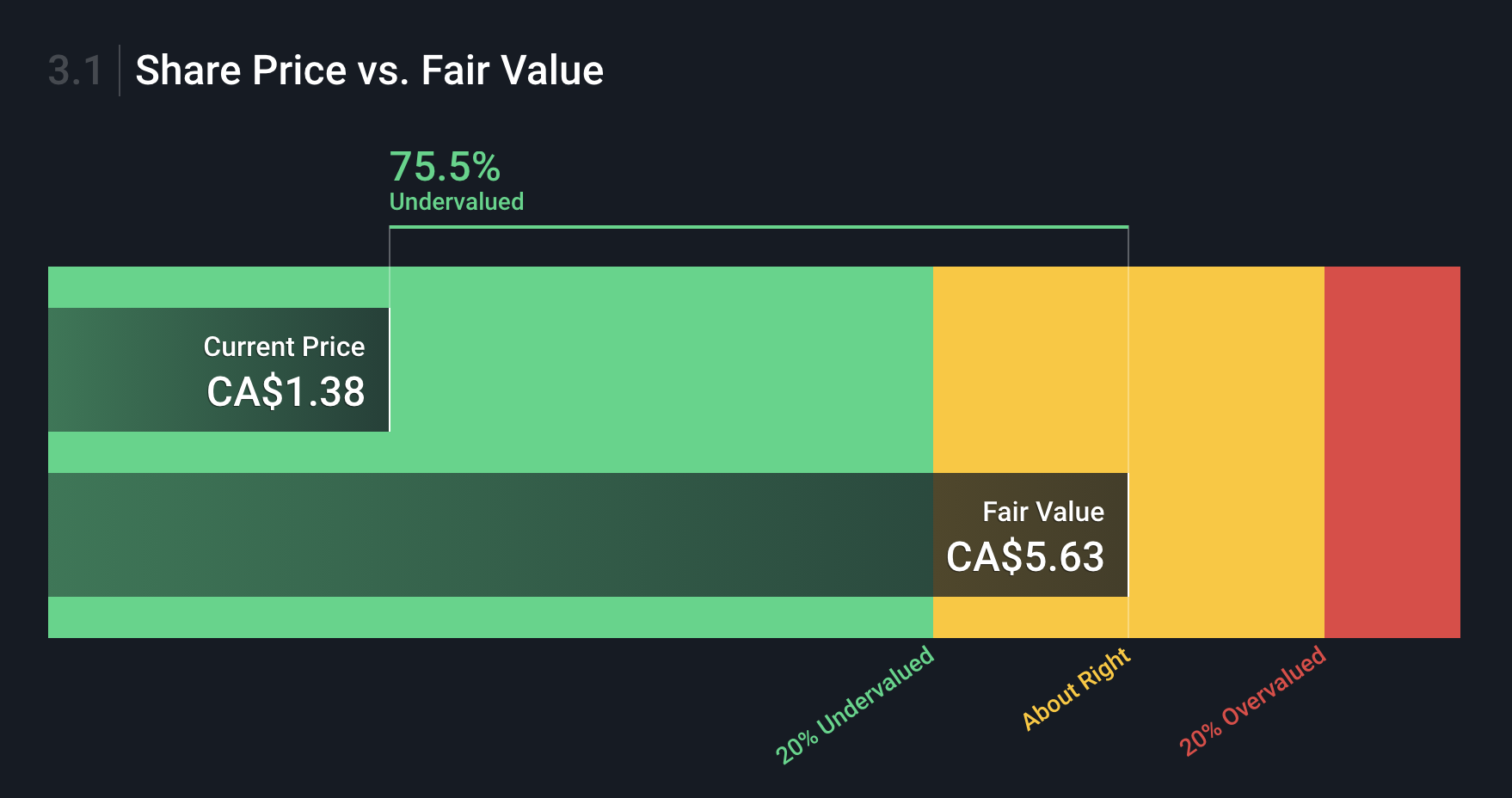

Stock Performance, Valuation

Popreach has grown 64.29% since its IPO on 11 October 2019. There’s a broad consensus that the stock is undervalued, firms such as Echelon and AI platforms such as Simply Wall St. have valued the company well above its stock price.

Source: Simply Wall Street (January 11-2021)

Risk of dilution

Although the company only has 73, 008 shares outstanding Popreach will need to issue additional equity on a continuous basis in order to keep acquiring companies. Popreach is already at a negative debt to equity ratio of -312%, which poses a serious risk to current holders.

Pearl Gray’s take

We’re impressed with the core revenue figures and cost-cutting capabilities of the company. In addition, we see this stock as an asset, which produces both value and growth.

Although Popreach does pose a serious liquidation risk, the company does fall within our mandate and we’ll be buying the stock before Q2-2021.

Disclosure: We hold a long position in the stock and this isn't financial advice.